National Strategy For Financial Inclusion

- 11 Jan 2020

- On 10th January, 2020, the Reserve Bank of India (RBI) released the five year (2019-24) National Strategy for Financial Inclusion (NSFI) with an objective to include all under formal access to finance - a key goal of the government.

- The NSFI sets forth the vision and key objectives of the financial inclusion policies in India to help expand and sustain the financial inclusion process at the national level through a broad convergence of action involving all the stakeholders in the financial sector.

Aim

- To provide access to formal financial services in an affordable manner.

- To broaden the financial inclusion and promoting financial literacy and consumer protection.

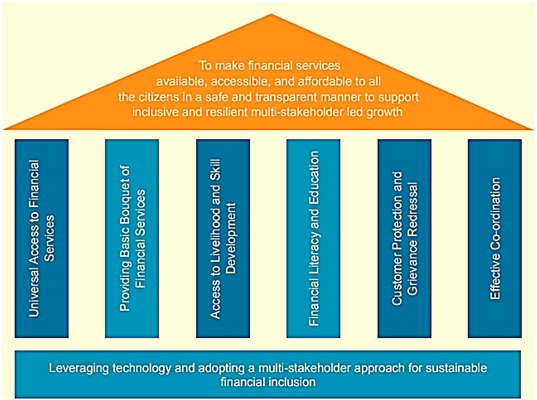

Strategic Pillars of National Strategy for Financial Inclusion

Strategic Pillars of National Strategy for Financial Inclusion

Recommendations

Universal Access to Financial Services

- The digital infrastructure in the country needs to be expanded through better networking of bank branches, BC outlets, Micro ATM, PoS terminals and stable connectivity, etc. coupled with electricity. Efforts are needed to be undertaken through co-ordination with various stake holders to ensure creation of the requisite infrastructure for moving towards completely digital on-boarding of customers.

- Encourage adoption and acceptance for digital payments and bringing people into the fold of formal financial system.

- Some of the issues such as remuneration to the Business Correspondents (BCs), need for furnishing cash-based collaterals, cash management issues and lack of insurance for cash in transit which act as deterrents in smooth functioning of the BC network, need to be redressed by banks in a timely manner.

Providing Basic Bouquet of Financial Services

- The banks may undertake periodic review of their existing products and adopt a customer centric approach while designing and developing financial products.

- Ensure efficient delivery by leveraging on Fin-tech and BC network.

- Initiate measures for capacity building of the BCs by encouraging and incentivizing them to acquire requisite certifications and enabling them to deliver a wide range of financial products.

- Make the Public Credit Registry (PCR) fully operational so that authorised financial entities can leverage on the same for assessing credit proposals from all citizens.

Access to Livelihood and Skill Development

- There should be convergence of objectives of the National Rural Livelihood and Urban Livelihood Missions to deepen financial inclusion through an integrated approach.

- Inter-linkages may be developed between banks and other financial service providers with ongoing skill development, and livelihood generation programmes through RSETIs, NRLM, SRLM, Pradhan Mantri Kaushal Vikas Yojana, etc.

Financial Literacy and Education

- Concerted efforts are needed to ensure coordination among the ground level functionaries Lead District Manager (LDM), District Development Manager (DDM) of NABARD, Lead District Officer (LDO) of RBI, District and Local administration, Block level officials, NGOs, SHGs, BCs, Farmers’ Clubs, Panchayats, PACS, village level functionaries, etc. while conducting financial literacy programmes.

Customer Protection and Grievance Redressal

- A robust customer grievance redressal mechanism at different levels helps banks in timely redressal of grievances.

- Develop a portal to facilitate inter-regulatory co-ordination for redressal of customer grievance.

Effective Co-ordination

- Strengthen the various fora under Lead Bank Scheme to ensure the achievement of the vision of the strategy at the ground level.

- Leverage on the emerging developments in technology to promote effective stakeholder co-ordination by having in place a digital dashboard/ MIS monitoring.

- Encourage decentralized approach to planning and development by creating a forum to actively involve Gram Panchayats/ Civil Society/ NGOs to accelerate financial inclusion using various tools like social audit.

What is Financial Inclusion?

- Financial inclusion is defined as the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost.

- It is also noteworthy to state that, seven of the seventeen United Nations Sustainable Development Goals (SDG) of 2030 view financial inclusion as a key enabler for achieving sustainable development world wide by improving the quality of lives of poor and marginalized sections of the society.

Causes of Financial Exclusion in India

- Lack of surplus income

- Not suitable to customer’s requirements

- Lack of requisite documents

- Lack of awareness about the product

- Lack of trust in the system

- High transaction costs

- Remoteness of service provider

- Poor quality of services rendered

Challenges to Financial Inclusion

Despite the various measures that have been undertaken by various stakeholders in strengthening financial inclusion in the country, there are still critical gaps existing in the usage of financial services that require attention of policy makers through necessary co-ordination and effective monitoring.

- Inadequate Infrastructure: Limited physical infrastructure, limited transport facility,inadequately trained staff, etc., in parts of rural hinterland and far-flung areas of the Himalayan and North-East regions create a barrier to the customer while accessing financial services.

- Poor Connectivity: Still many regions in the country have poor connectivity tend to be left behind in ensuring access to financial services there by creating a digital divide. Certain communities are likely to be excluded where electricity is not available, hardware is in short supply or networks are limited.

- Socio-Cultural Barriers: Prevalence of certain value system and beliefs in some sections of the population results in lack of favourable attitude towards formal financial services. There are still certain groups (especially women) who do not have the freedom and choice to access financial services because of cultural barriers.

- Monopoly in Payment Infrastructure: Currently, majority of the retail payment products viz., CTS, UPI, IMPS, etc. are operated by National Payments Council of India (NPCI), a Section (8) Company promoted by a group of public, private and foreign banks. There is a need to have more market players to promote innovation and competition and to minimize concentration risk in the retail payment system from a financial stability perspective.

- Security Concerns: Given the increasing reliance on technology to deliver banking services to customers, it is essential that adequate attention is paid to security, especially IT security. Security related issues resulting in frauds potentially undermine public confidence in the use of electronic payment products. Further, they could also lead to reputation risks.

- Low Levels of Financial Literacy: A low level of financial literacy is often a hidden hurdle to bringing financial inclusion to the unbanked. Poor knowledge of how products work and their likely costs also reduce the likelihood of inclusion. The same issues may also prevent individuals from making full use of their existing products.

Way Forward

- Financial inclusion is increasingly being recognized as a key driver of economic growth and poverty alleviation the world over. Access to formal finance can boost job creation,reduce vulnerability to economic shocks and increase investments in human capital.

- Without adequate access to formal financial services, individuals and firms need to rely on their own limited resources or rely on costly informal sources of finance to meet their financial needs and pursue growth opportunities. At a macro level, greater financial inclusion can support sustainable and inclusive socio-economic growth for all.