Economic Nobel 2022: An Insight to avoid both Serious Crises and Expensive Bailouts

- 11 Oct 2022

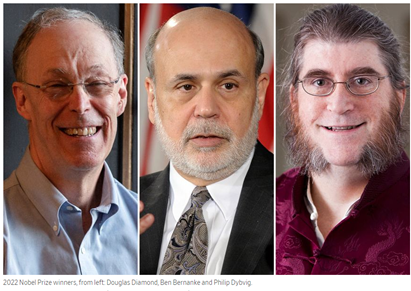

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2022 was awarded to Ben S. Bernanke, Douglas W. Diamond, Philip H. Dybvig (all from the USA) “for research on banks and financial crises”.

- Together, the work for which Bernanke, Dybvig and Diamond have been recognised has also laid the foundation for modern bank regulations. Their work has been “crucial to subsequent research that has enhanced our understanding of banks, bank regulation, banking crises and how financial crises should be managed”.

- They have demonstrated the importance of preventing widespread bank collapses that also gives an insight to avoid both serious crises and expensive bailouts.

(Image Source: WSJ)

Diamond and Dybvig’s Analysis

Since the Global Financial Crisis of 2008, banks have lost their sheen in the public eye. They are often seen as money-grabbing institutions that exist to profit off borrowers as well as depositors.

But in a world without banks, it would be impossible to make any long-term investment. That’s because, as Diamond and Dybvig’s 1983 paper showed, there are “fundamental conflicts between the needs of savers and investors”.

Savers-Investors Conflict

- Savers always want access to at least some part of their savings for unexpected use; this is also called the need for liquidity. They want the ability to pull out money when they need it.

- Borrowers, especially those taking out a loan for building a home or building a road, need the money for a much longer time. Borrowers cannot function if the money can be demanded back at a short notice.

Resolving this Mismatch

- Diamond and Dybvig showed that these mismatches can best be solved by institutions constructed exactly like banks.

- They developed a theoretical model that explains how banks create liquidity for savers, while borrowers can access long-term financing.

|

Maturity Transformation Diamond and Dybvig explained that banks are able to resolve Savers-Investors conflict through the process of maturity transformation.

Role of Maturity Transformation

Role of Assets & Liability

|

Banks as an Intermediaries in Crisis

- Their analysis also showed how the combination of these two activities (savings and lending) makes banks vulnerable to rumours about their imminent collapse.

- If a large number of savers simultaneously run to the bank to withdraw their money, the rumour may become a self-fulfilling prophecy – a bank run occurs and the bank collapses.

Scrutinizing Investments

- Diamond demonstrated how banks perform another societally important function. As intermediaries between many savers and borrowers, banks are better suited to assessing borrowers’ creditworthiness and ensuring that loans are used for good investments.

Ben Bernanke’ Analysis: Bank Run

Ben Bernanke analysed the Great Depression of the 1930s, the worst economic crisis in modern history. Among other things, he showed how bank runs were a decisive factor in the crisis becoming so deep and prolonged.

What is Bank Run?

- Bank runs happen when depositors become worried about the bank’s survival, and rush to withdraw their savings.

Effects of Bank Run

- Bankruptcy: If enough people withdraw their money simultaneously, the bank’s reserves cannot cover all the withdrawals, and it is driven to bankruptcy.

- Productive Investments are hampered: When the banks collapsed, valuable information about borrowers was lost and could not be recreated quickly. Society’s ability to channel savings to productive investments was thus severely diminished.

Finally Financial Crisis Decoded

- Until Bernanke’s paper, bank failures were seen as a “consequence” of the financial crisis. But Bernanke’s 1983 paper proved it was exactly the opposite— bank failures were the “cause” of the financial crisis.

- Using a combination of historical sources and statistical methods, his analysis showed which factors were important in the drop in GDP. He found that factors that were directly linked to failing banks accounted for the lion’s share of the downturn.

Remedy Options

- Bernanke demonstrated that the economy did not start to recover until the state finally implemented powerful measures to prevent additional bank panics.

- The deposit insurance provisions — where a certain amount of one’s deposits in a bank are insured — is a critical tool towards building trust and preventing bank runs.

|

How Reserve Bank of India addresses the Issue of Bank Failure

Recent Govt. Interventions towards Bank Deposit Insurance Programme

|