National Strategy For Financial Education

- 24 Aug 2020

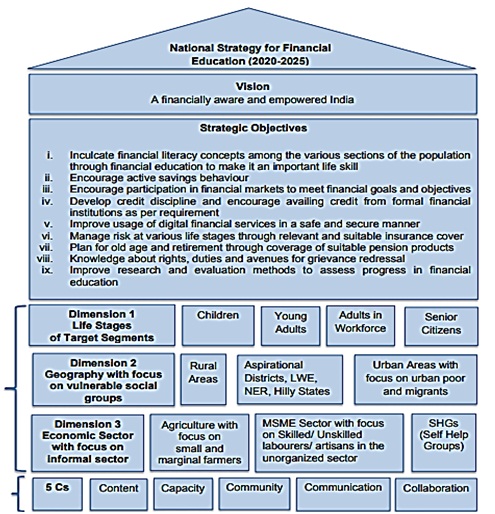

- On 20th August, 2020, the Reserve Bank of India (RBI) released the National Strategy for Financial Education(NSFE): 2020-2025 document in order achieve the vision of creating a financially aware and empowered India.

- This is the second national strategy; the first NSFE was launched in 2013.

Background and Rationale of NSFE

- India has a large population of adults.This demographic advantage can beleveraged to ensure that India becomes one of the fastest growing economies, with emphasis on inclusive growth through a vibrant and stable financial system.

- Over the last few years, there has been rapid progress towards digitalization which has brought newer opportunities to the forefront like never before.

- There is a paradigm shift in digital transactions and Payment Infrastructure in the country (Goal of Less Cash Economy). Due to all these developments, it has become imperative to revise the existing National Strategy for Financial Education (NSFE) and to adopt innovative measures to implement the same.

- Towards this objective, the National Centre for Financial Education (NCFE) has been set up by all the Financial Sector Regulators as a Section (8) company under Companies Act, 2013 to undertake basic financial education and to develop suitable content for increasing financial literacy among the masses in the country.

Strategic Objectives of NFSE

- Inculcate financial literacy concepts among the various sections of the population through financial education to make it an important life skill.

- Encourage participation in financial markets to meet financial goals and objectives.

- Develop credit discipline and encourage availing credit from formal financial institutions as per requirement.

- Improve usage of digital financial services in a safe and secure manner.

- Manage risk at various life stages through relevant and suitable insurance cover.

- Knowledge about rights, duties and avenues for grievance redressal.

Major Highlights

- This NSFE has been prepared by the National Centre for Financial Education (NCFE) in consultation with all the Financial Sector Regulators viz. RBI, Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), etc. under the aegis of the Technical Group on Financial Inclusion and Financial Literacy (TGFIFL).

- To prepare a comprehensive Strategy based on people’s needs and the country’savailable resources, the following process has been adopted in the Indian context:

- Assessing and evaluating gaps in financial literacy.

- Comparison of NSFE with the OECD International Network on Financial Education(OECD-INFE) Policy Handbook on National Strategies for Financial Education.

- It focuses on advancement of skills of financial service providers and other intermediaries involved in dissemination of financial literacy.

- It intends to support the vision of the Government of India and the Financial Sector Regulators by empowering various sections of the population to develop adequate knowledge, skills, attitudes and behaviour which are needed to manage their money better and to plan for the future.

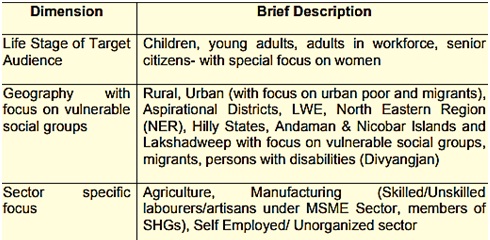

- The Strategic Objectives are envisaged to be achieved through the following dimensions-

Key Recommendations

- In order to achieve the Strategic Objectives laid down, the document recommends adoption of a ‘5 C’ approach-

Content

- Financial Literacy content for school children (including curriculum and co-scholastic), teachers, young adults, women, new entrants at workplace/ entrepreneurs (MSMEs), senior citizens, persons with disabilities, illiteratepeople, etc.

Capacity

- Develop the capacity of various intermediaries who can be involved in providing financial literacy.

- Develop a ‘Code of Conduct’ for financial education providers.

Community

- Evolve community led approaches for disseminating financial literacy in asustainable manner.

Communication

- Use technology, mass media channels and innovative ways of communicationfor dissemination of financial education messages.

- Identify a specific period in the year to disseminate financial literacy messageson a large/ focused scale.

- Leverage on Public Places with greater visibility (e.g. Bus Stands, RailwayStations, etc.) for meaningful dissemination of financial literacy messages.

Collaboration

- Preparation of an Information Dashboard.

- Streamline efforts of other stakeholders for financial literacy.

- The Strategy also suggests adoption of a robust ‘Monitoring and Evaluation Framework’ to assess the progress made under the Strategy.

Expected Impact

- The strategy will develop credit discipline and encourage availing credit from formal financial institutions as per requirement. It will improve usage of digital financial services in a safe and secure manner.

- Besides encouraging active savings behavior, it will encourage participation in financial markets to meet financial goals and objectives.

- It will help improve research and evaluation methods to assess progress in financial education.

|

OECD/INFE Policy Handbook on National Strategies for Financial Education

Four Key Policy Areas Related to Financial Education

|

About Financial Education

- Financial Education is defined as the process by which financial consumers/investors improve their understanding of financial products, concepts and risks and through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, to make informed choices, to know where to go for help and to take other effective actions to improve their financial well-being.

- While, Financial Literacy is defined as a combination of financial awareness, knowledge, skills, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being.

|

OECD-INFE Definition of Components of Financial Literacy

|

Components of Financial Education

Basic Financial Education

- The basic financial education consists of fundamental tenets of financial well-being.With the introduction of Government’s Pradhan Mantri Jan DhanYojana (PMJDY) scheme along with APY, PMJJBY &PMSBY besides MUDRA Yojana, many people have already been included. They alsorequire financial education so that they can take full benefits from these schemes.

- These basic concepts need to be communicated to everyone by adopting different modes ofdelivery, suitable to the target audience.

- Special emphasis shall be laid on the financially excluded and those newly included but not operating their accounts.

- The basic financialeducation acts as a foundation for sector-specific and process education.

Sector Specific Financial Education

- Sector specific financial education is being imparted by the Financial Sector Regulators and focuses on “What” of the financial services and the contents cover awareness on ‘Do’s & Don’ts’, ‘Rights & Responsibilities’, ‘Safe usage of digital financial services’ and approaching ‘Grievance Redressal’ Authority.

Process Education

- Process education is crucial to ensure that the knowledge translates into behavior.

Way Forward

- Financial education plays a vital role in creating demand side response to the initiatives of the supply side interventions.

- Incidentally, financial education also supports achievement of Sustainable Development Goal (SDG) No. 4 on Education which aims to ensure inclusive and equitable quality education and promote life-long learning opportunities for all (SDG Target 4.6 on Literacy and SDG Target 4.4 on Life Skills under SDG 4 on Education).

- Financial education initiatives by concerned stakeholders will help people achieve financial well-being by accessing appropriate financial products and services through regulated entities.

- There is a need to increase the size of banking as well as other financial sectors to ensure that the benefits of these developments reach the common masses.

- Keeping in view the vast and rapid changes taking place in the financial sector, all the stakeholders need to appreciate the dynamic nature of evolution of financial services and the concomitant changes that are required towards financial literacy.

- Arobust and scientific assessment method would go a long way in helping Policy makers identify priorities and assess the impact of their interventions.

- Some of the broad issues that need to be considered in this regard are as under:

- National Strategy evaluation to include an assessment of the governance, co-ordination and monitoring mechanisms of the implementation methods, the role of stakeholders and the effects of any communication or publicity plans/ initiatives.

- Each stakeholder needs to clearly plan and articulate their role in the design, development and implementation of the Strategy which shall be monitored through qualitative and quantitative indicators.

- A scientifically designed template for gathering feedback through various channels, from both the beneficiaries of financial literacy programmes and the intermediaries involved in disseminating the same, needs to be prepared and periodically reviewed keeping in view the vast changes in the financial sector.

- Selection of appropriate evaluation methods need to be finalized in view of the challenges involved in evaluation.