K V Kamath Committee Report On ‘Resolution Framework For Covid-19 Related Stress’

- 10 Sep 2020

- On 7th September, 2020,the Reserve Bank of India (RBI) released a report by the K V Kamath Committee which was formed to make recommendations on the required financial parameters to be factored in the resolution plans under the ‘Resolution Framework for Covid-related Stress’, along with sector specific benchmark ranges for such parameters.

Key Highlights

- The Committee recognizes that:

- The Covid-19 pandemic has affected the best of companies.

- These businesses were otherwise viable under pre-Covid-19 scenario.

- Impact is pervasive across several sectors but with varying severity – mild, moderate and severe.

- The committee has recommended financial parameters including aspects related to leverage, liquidity and debt serviceability.

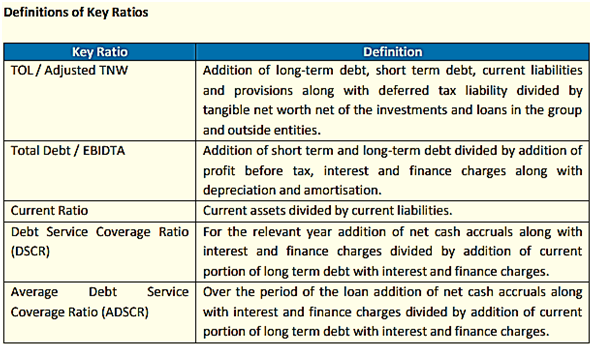

- It selected five parameters based on their relevance while considering the resolution plan(RP).These ratios would provide the requisite assessment framework for the RP. These include:

- Total Outside Liability/Adjusted Tangible Net Worth (TOL/Adjusted TNW)

- Total Debt/EBIDTA

- Current Ratio

- Debt Service Coverage Ratio (DSCR)

- Average Debt Service Coverage Ratio (ADSCR)

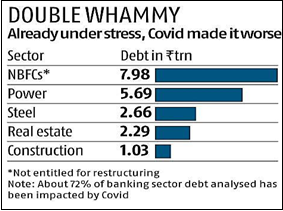

- It suggested financial ratios for 26 sectors which could be factored by lending institutions while finalising a resolution plan for a borrower. These sectors include aviation, hospitality, real estate which are some of the most stressed sectors in the economy due to the impact of Covid-19 pandemic.

Source: Business Standard

Source: Business Standard

- Considering the large volume and the fact that only Standard assets are eligible under the proposed scheme, a segmented approach of bucketing these accounts under mild, moderate and severe stress, may ensure quick turnaround.

- To complete this task simplified restructuring for mild and moderate stress may be prescribed. Severe stress cases would require comprehensive restructuring.

Key Recommendations on Sector Specific Parameters

- The sector specific parameters may be considered as guidance for preparation of RP for a borrower in the specified sector.

- The RP may be prepared based on the pre-Covid-19 operating and financial performance of the borrower and impact of Covid-19 on its operating and financial performance in Q1 and Q2FY21, to assess the cash-flows for FY21 / FY22 and subsequent years. In these financial projections, the threshold TOL/Adjusted TNW and Debt/ EBIDTA ratios should be metby FY23.

- The other three threshold ratios should be met for each year of the projections starting from FY22. The base case financial projections need to be prepared as part of RP.

- In respect of those sectors where the threshold parameters have not been specified by the Committee, lenders can make their own internal assessments for the solvency ratios i.e. TOL/Adjusted TNW and Total Debt/EBIDTA. However, the current ratio and DSCR shall be 1.0 and above, and ADSCR shall be 1.2 and above.

- The Committee has uniformly proposed thresholds for current ratio, DSCR and ADSCR in most of the sectors.

- The borrowers eligible under the current Framework are Standard Accounts and as such, they may require some time to restore their position to pre-Covid-19 levels.

- As per the recommendations, the resolution process should be treated as invoked once lenders representing 75 percent by value and 60 percent of lenders agree to do so.

Analysis

- According to the experts, the K V Kamath panel's loan recast recommendations are better than the erstwhile corporate debt restructuring (CDR) mechanism, but these may result in banks postponing recognition of stress through short-term relief.

- The CDR was extensively used to suppress non-performing assets and had a success rate of as low as 15 percent.

- The framework is for a limited time-period and stresses upon upfront heavy provisioning, stringent financial thresholds for eligibility and supervisory mechanism.

- In the absence of an economic revival and sector-specific packages to be introduced by the government, the new mechanism will be "challenging" and may also end up induce uncertainty in the credit markets as banks focus on working out the recast plans in the limited window.

- Stressed borrowers in real estate, traders, hotels/restaurants segments will be helped, but resolving stress in lumpy power and infrastructure sectors through this mechanism will be challenging without economic revival and sector-specific packages or initiatives by the government.

- It is feared a "good portion" of the accounts which will be restructured will eventually turn non-performing and added that it gives a ""short-term relief" alone.

- The framework is much broader than anticipated but leaves some scope for subjectivity as thresholds are to be met 2021-22 onwards based on base-case financial projections.