The Chit Funds (Amendment) Bill, 2019

- 30 Nov 2019

- On 28th November, 2019, the Rajya Sabha passed the Chit Funds (Amendment) Bill, 2019, aimed at reducing the compliance burden on chit funds and protecting subscribers that primarily comprises economically weaker sections of the society.

- The Bill was passed by Lok Sabha on 20th November, 2019.

- It seeks to amend the Chit Funds Act, 1982, which regulates chit funds and prohibits a fund from being created without prior sanction of a state government.

Objectives

- To facilitate orderly growth of the chit fund sector and streamline operations of collective investment schemes or chit funds

- To remove bottlenecks being faced by the chit fund industry

- To enable greater financial access to people

Need for Bill

- To Protect Investor’s Interest: The need to protect investor interest highlights the crucial role chit funds play in India’s rural economy, providing people with access to funds and investment opportunities, especially in regions where banks and financial institutions do not have a presence.

Salient Features of the Bill

Substitution of Terms

- The Bill substitutes the words chit amount, dividend and prize amount with gross chit amount, share of discount and net chit amount,

- It has introduced words such as ‘fraternity fund’, ‘rotating savings’ and ‘credit institution’ to help these funds get an image makeover, and build a brand for them.

- In addition, it recognizes chit funds under various names, including kuri, fraternity fund, rotating savings, credit institution.

Increase in Aggregate Amount of Chits

It proposes to increase the maximum amount of chit funds which may be collected by:

- Individuals: from Rs. 1 lakh to Rs. 3 lakh

- Firms: from Rs. 6 lakh to Rs. 18 lakh.

Presence of Subscribers through Video-Conferencing

- It mandates that at least two subscribers must be present, either physically or via video-conferencing, when a chit is drawn.

Foreman's Commission

- It proposes to raise the maximum commission of a foreman from 5% of the chit amount to 7%.

- Further, the Bill allows the foreman a right to lien against the credit balance from subscribers. (A foreman is simply the manager of the chit fund)

Applicability

- The principal Act does not apply to any chit started before it was enacted or to any chit where the amount is less than Rs 100.

- The Bill seeks to remove the limit of Rs 100, and allows the state governments to specify the base amount over which the provisions of the Act will apply.

Impact

- Ensuring Accountability and Transparency: The provision in the bill to allow subscribers to be present through video conferencing would increase transparency and accountability in managing chit funds.

- Making Chit Funds Investor Friendly: It will help in safeguarding the people subscribing to the scheme as it provides for the chit fund operator to have secured deposit to the size of the scheme, thus making chit funds investor friendly.

Chit Funds

- Chit fund is a traditional financing system practiced in India wherein a few people (known as members or subscribers) come together and invest a fixed amount every month for a fixed period.

- It provides assistance to those who are looking at an alternate to money lenders and the stringent procedures followed by banks.

- During the process of collection, any member can draw a lump sum through various ways like a lucky draw, an auction or a member can even fix a payout date based on a known expenditure.

- Although the system exists in other parts of the world by the name Rotating Savings and Credit Association (ROSCA), India is the only country where its operations are governed by legislations.

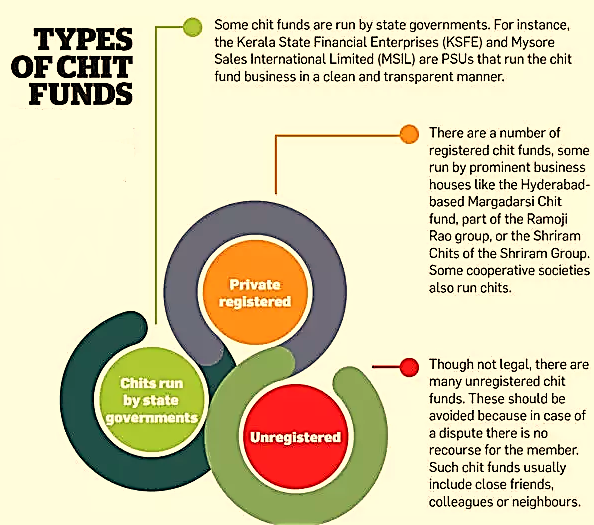

Types of Chit Funds

In India there are three types of chit funds, namely:

- Funds run by state governments;

- Private registered chit funds; and

- Unregistered chit funds.

Source: ET

Difference between Chit Funds and Ponzi Schemes

|

Advantages

- Provides flexibility to borrow and save. One get a chance to borrow money (pot) just by paying first monthly installment.

- Best option of finance for needy people, without any documents like IT returns, PAN card etc.

- Chit fund is a good savings instrument and it can be a reliable source of funds in an emergency.

- Intermediation cost is the lowest when compared to other instruments.

Disadvantages

- Chit-funds do not offer any pre-determined or fixed returns.

- Chances of fraud are high suppose foreman run away with corpus amount.

- A winning subscriber may disappear after winning the first bid.

- The subscriber may default and not ready to pay next installments.

- High degree of risk with very little protection

Way Forward

- Chit funds are popular among low-income group people as it offers them the opportunity to save and invest. It is an excellent tool to promote financial inclusion, if channelized in the right format.

- However, archaic legislations have made it impossible for the chit fund industry to adopt technology and move to a system of e-auctions and e-payments because of the insistence of “physical presence” required as per Sections 16 of the Chit Fund Act.

- It is high time that policymakers review their apathy for the chit fund industry to redesign and modernize the legislation that regulates this widely spread financial practice.